Smart Ways to Handle Insurance and Medical Costs After Treatment

You probably feel overwhelmed by medical bills after treatment. Many people worry about paying large bills or even going into debt. You might use savings, borrow money, or cut back on things like food and clothes. Surveys show that over half of adults in the USA face these struggles. Staying organized and proactive helps you tackle Financial Challenges - Navigating Insurance and Cost After Treatment without extra stress.

Some people delay care because of costs

Many experience anxiety about bills

Key Takeaways

Stay organized by tracking your medical bills and insurance paperwork. This helps you avoid overpaying and reduces stress.

Review your medical bills carefully. Many contain errors that can cost you money. Always ask for an itemized bill to check for mistakes.

Communicate effectively with your healthcare providers and insurance companies. Write down your questions and ask for clear explanations.

Explore financial assistance programs. Many organizations offer help with medical costs, transportation, and lodging for treatment.

Consider working with financial counselors or patient advocates. They can help you navigate bills, negotiate costs, and find financial aid.

Financial Challenges - Navigating Insurance and Cost After Treatment

After treatment, you might feel lost when it comes to handling bills and insurance. The Financial Challenges - Navigating Insurance and Cost After Treatment can seem endless. You may see unexpected charges, confusing paperwork, and high out-of-pocket costs. Many people struggle to understand what their insurance covers or how to manage ongoing expenses. Here are some of the main challenges you could face:

Understanding insurance coverage and what it really pays for

Managing out-of-pocket expenses that add up quickly

Dealing with the complexity of the healthcare system

Facing high medical bills, even if you have insurance

Handling the long-term impact of ongoing care

Paying for new technology or treatments

Keeping up with costs for chronic conditions

Navigating economic factors that affect treatment prices

Why Post-Treatment Cost Management Matters

You might wonder why you should focus on managing costs after treatment. Taking charge now can help you avoid bigger problems later. If you stay proactive, you can save money and protect your financial future. Studies show that people who take steps to manage their health and costs can save thousands of dollars. For example:

Proactive health steps can save over $500 billion each year for programs like Medicare.

Healthy habits can delay serious illnesses, which means fewer bills and less stress.

Preventive care can slow down rising healthcare costs without cutting benefits.

If you ignore the Financial Challenges - Navigating Insurance and Cost After Treatment, you risk falling into debt or missing out on important care.

Tip: Start by tracking your bills and insurance paperwork. This small step can make a big difference.

Common Financial Pitfalls

Many people make mistakes when dealing with the Financial Challenges - Navigating Insurance and Cost After Treatment. Here are some common pitfalls:

Not reviewing bills carefully, which can lead to overpaying because of errors

Ignoring chances to negotiate bills or ask for discounts

Missing out on financial help from hospitals or charities

Using high-interest credit cards to pay medical bills, which can create more debt

Delaying or skipping care because of money worries

Feeling anxious or stressed, which can affect your mental health

Struggling to pay other bills, which can lead to housing problems

Here’s a quick look at how medical debt can affect your life:

Impact of Medical Debt | Description |

|---|---|

Medical debt can lead to ongoing financial struggles, making it harder to pay off other debts. | |

Credit Score Impact | Unpaid medical bills can negatively affect credit scores for up to seven years. |

Access to Healthcare | Individuals with medical debt are less likely to seek necessary healthcare services. |

You can avoid many of these problems by staying organized and asking for help when you need it. Facing the Financial Challenges - Navigating Insurance and Cost After Treatment head-on gives you more control and peace of mind.

Review and Understand Your Medical Bills

After treatment, you might get a stack of papers in the mail. Some are bills, and some are insurance forms. It can feel confusing, but you can take control by checking everything closely. This step helps you avoid paying more than you should and keeps you on top of the Financial Challenges - Navigating Insurance and Cost After Treatment.

Checking for Accuracy

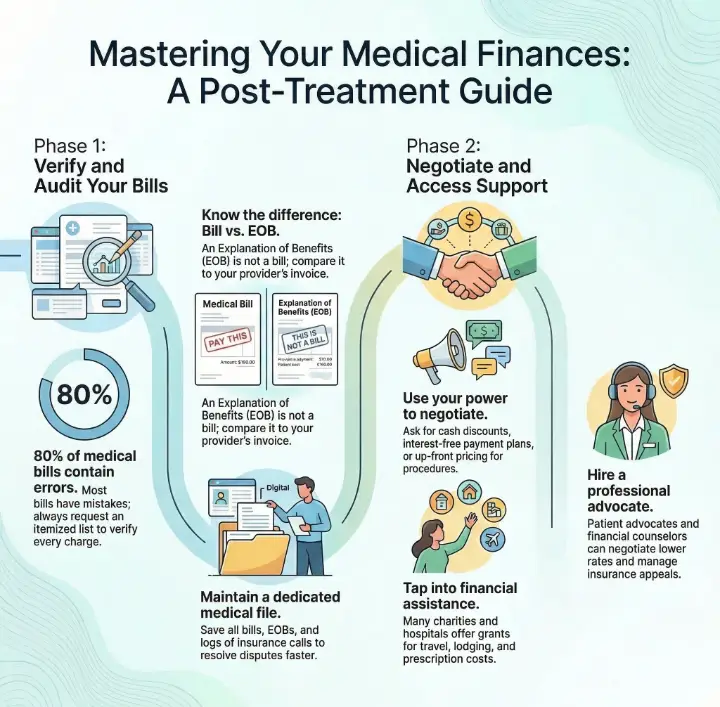

Did you know most medical bills have mistakes? Studies show that about 80% of bills contain errors or unexpected charges. Sometimes, these mistakes can cost you hundreds or even thousands of dollars. Here’s a quick look at what recent studies found:

Source | Statistic |

|---|---|

AKASA | 80% of medical bills contain at least minor mistakes |

BillFlash | Approximately 80% of U.S. medical bills contain some kind of error |

American Medical Association | Up to 12% of medical claims are submitted with inaccurate codes |

Dialog Health | Average hospital bill over $10,000 has errors amounting to around $1,300 in overcharges |

You can protect yourself by following these steps:

Review every bill for mistakes, like wrong numbers or codes.

Ask for an itemized list of charges and compare it with your records.

Make sure your providers have your current contact and insurance details.

Track your out-of-pocket maximum and check it against your insurance records.

Wait for your Explanation of Benefits (EOB) before you pay anything.

Tip: If you spot something that doesn’t look right, call your provider or insurance company. Ask questions until you understand every charge.

Understanding EOBs and Claims

You might wonder what all these papers mean. A medical bill and an Explanation of Benefits (EOB) are not the same thing. Here’s a simple table to help you tell them apart:

Aspect | Medical Bill | Explanation of Benefits (EOB) |

|---|---|---|

Source | From the health care provider | From the health insurance company |

Content | Shows what you need to pay | Lists charges, what insurance paid, and what you owe |

Identification | Usually just looks like a bill | Clearly says “THIS IS NOT A BILL” |

When you understand your bills and EOBs, you can spot errors and avoid paying too much. This helps you stay ahead of the Financial Challenges - Navigating Insurance and Cost After Treatment.

Confirm Insurance Coverage and Resolve Issues

Identifying Coverage Gaps

You might think your insurance covers everything, but sometimes it does not. Coverage gaps can surprise you with extra bills. Start by reading your insurance policy. Look for what is included and what is not. Check if your treatment, medicine, or follow-up visits fall under your plan. If you see a service not covered, call your insurance company. Ask them to explain why. Sometimes, a simple mistake causes a gap. You can also ask your doctor’s office to help you understand your benefits.

Here are some steps you can take to spot coverage gaps:

Review your policy’s summary of benefits.

Compare your bills with your insurance statements.

Ask your provider for a pre-authorization letter for future treatments.

Keep notes of every call or email with your insurance company.

If you find a gap, do not panic. Many people face Financial Challenges - Navigating Insurance and Cost After Treatment because of these surprises. Stay calm and ask questions until you understand your options.

Addressing Billing Errors

Billing errors happen more often than you think. You might see charges for services you did not get or find the same charge twice. Sometimes, a wrong code leads to a big bill. You can fix these mistakes if you know what to look for.

Here are some best practices for resolving billing errors:

Strategy | Description |

|---|---|

Review claims before payment to spot errors and negotiate fair prices. | |

Line-Item Bill Review | Check each item on your bill to make sure it matches the care you received. |

Understanding Billing Errors | Learn about common mistakes like data entry errors or wrong codes. |

Claims negotiation helps you catch and fix mistakes before you pay.

Line-item bill reviews make sure you only pay for what you received.

Knowing about common billing errors can save you money.

If you find an error, call your provider or insurance company. Ask them to explain the charge. Write down who you spoke with and what they said. Keep copies of all your bills and letters. This way, you stay organized and ready to solve any problem.

Negotiate and Manage Medical Costs

Medical bills can feel scary, but you have more power than you think. You do not have to accept every bill at face value. Many providers expect you to ask questions or even negotiate. Let’s look at how you can take control and lower your costs.

When and How to Negotiate Bills

You can start negotiating your bills as soon as you get them. Many people do not realize that hospitals and clinics often have room to lower prices, especially if you ask. Here are some smart ways to begin:

Call the billing office and ask if they offer discounts for paying in cash.

Request an itemized bill so you can see every charge.

Point out any errors or duplicate charges.

Ask if they have charity care programs or financial assistance.

Offer to pay a portion up front in exchange for a lower total.

You can also try to negotiate before you get care, especially for non-emergency tests or procedures. Providers may give you a better price if you ask for it ahead of time.

Tip: Always stay polite and calm. The person on the phone wants to help you, but they may need to check with a supervisor.

Here’s a table showing some of the most effective strategies for negotiating medical bills:

Strategy | Description |

|---|---|

Claims Negotiation | Work directly with providers to find billing errors and use pricing data to lower your bill. |

Line-Item Bill Review | Go through each charge to make sure you only pay for what you received. |

You can also try these steps:

Negotiate with healthcare providers before you get care.

Ask for up-front pricing for tests and procedures.

Inquire about discounts, like cash payment or charity care.

Payment Plans and Discounts

If you cannot pay your bill all at once, do not panic. Most hospitals and clinics offer payment plans. These plans let you pay a little each month, often with no interest. Here’s how you can set one up:

Call the billing office and explain your situation.

Ask about payment plan options and how long you have to pay.

Make sure you understand the terms before you agree.

Get the agreement in writing.

You can also ask about discounts. Some providers give you a lower price if you pay in cash or pay quickly. Others have special programs for people with low incomes. Do not be afraid to ask, even if you think you might not qualify.

Note: If you get a big bill after an emergency, you may have legal protections. Laws can help you avoid surprise bills when you could not choose your doctor or hospital.

Claims Negotiation and Repricing

Sometimes, your insurance company does not pay as much as you expect. You might see a denied claim or a bill that seems too high. You can challenge these charges through claims negotiation and repricing. Here’s how the process usually works:

The provider sends a claim to your insurance company with all the details.

The insurance company checks the claim and compares it to their agreed rates.

If something looks wrong, they negotiate with the provider to lower the amount.

The final payment is set, and you get a report showing what was paid and what you owe.

You can help this process by keeping good records and checking every statement. If your claim gets denied, you have the right to appeal. Here are some steps you can take:

Keep clear records of all your bills and notes from your health plan.

Learn your insurance plan’s appeal steps and deadlines.

Provide good documentation when you appeal.

Ask your state’s insurance commissioner’s office for help if you need it.

Sometimes, you may need legal help. Attorneys can guide you through complex bills, fight insurance denials, and negotiate charges. You also have legal protections against surprise bills, especially after emergencies.

Callout: Do not give up if you get a denial or a high bill. Many people win appeals or get bills reduced just by asking and staying organized.

Negotiating and managing your medical costs takes effort, but you can do it. Each step you take helps you protect your finances and your peace of mind.

Use Financial Resources and Assistance

Health Savings and Emergency Funds

You can make a big difference in your medical finances by planning ahead. Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) help you set aside money for medical costs. These accounts let you pay for things like deductibles and copayments. You also get tax benefits, which means you keep more of your money. If you have a high-deductible health plan, an HSA gives you tax-free savings for medical expenses.

You should look at your insurance plan’s maximum out-of-pocket costs. Try to save enough to cover that amount. This way, you’re ready for any surprise bills. An emergency fund for healthcare helps you stay calm when unexpected costs pop up. You won’t have to scramble or borrow money if you have savings set aside.

Here are some ways you can gather funds for medical expenses:

Use your savings to pay bills.

Borrow money if you need to.

Cut back on things you don’t need.

Sell stocks or possessions for extra cash.

Move to a cheaper home if costs get too high.

Tip: Start small. Even saving a little each month adds up over time.

Government and Charity Programs

You don’t have to handle medical costs alone. Many programs offer help if you qualify. Some give free rides to treatment or free lodging if you travel for care. Others help pay for prescription medicines. You can also get support from programs like ACS CARES™, Social Security Disability Insurance, or Supplemental Security Income if you can’t work because of illness.

Check out this table for some helpful resources:

Resource | Description |

|---|---|

Free Rides to Treatment | Transportation help for getting to medical appointments. |

Free Lodging During Treatment | Places to stay if you need treatment far from home. |

ACS CARES™ | Support and guidance for cancer patients. |

Help Paying for Prescription Medicines | Assistance with medication costs. |

Social Security Disability Insurance | Financial support if you can’t work due to illness. |

Supplemental Security Income | Extra aid for low-income individuals with health issues. |

Government and charity programs also cover dental, optical, and prescription costs for seniors, children, and low-income families. Some programs, like GreenShield Cares and National Pharmacare, offer free medicines if you don’t have coverage. You can apply easily, and many programs don’t require tax filing.

Note: Ask your doctor or social worker about local programs. You might qualify for more help than you think.

Communicate with Providers and Insurers

Effective Communication Tips

Talking with your medical provider or insurance company can feel stressful. You might worry about saying the wrong thing or not getting the help you need. You can make things easier by using a few smart strategies. Start by writing down your questions before you call or visit. This helps you stay focused and not forget anything important.

You should always ask for clear explanations. If you do not understand a charge or a policy, ask the person to explain it in simple words. Do not feel shy about asking them to repeat or slow down. You have the right to know what you are paying for.

Here’s a table with some top strategies for working with providers and insurers:

Strategy | Description |

|---|---|

Claims Negotiation | Helps you find billing errors and lower your bill by talking directly with your provider. |

Line-Item Bill Review | Lets you check each charge for mistakes before you pay. |

Repricing by PPO Networks | Adjusts costs based on special agreements to help you save money. |

You can also try these tips:

Set up clear billing and coding rules with your provider.

Negotiate fair rates with your insurance company.

Stay updated on changes in healthcare billing.

Tip: Stay calm and polite. People are more willing to help when you treat them with respect.

Keeping Records

Good records help you avoid confusion and save money. You should keep every bill, letter, and email from your provider or insurance company. Use a folder, binder, or even a simple box to store your papers. Some people like to use a notebook or a phone app to track calls and emails.

Here are some easy ways to stay organized:

Use file folders or binders for all your medical bills and insurance letters.

Write down the date, time, and name of the person you spoke with.

Review every bill for mistakes before you pay.

Wait for your Explanation of Benefits (EOB) to make sure it matches your bill.

Keeping good records gives you proof if you need to dispute a charge. You will feel more confident and less stressed when you know where everything is.

Note: Staying organized can help you solve problems faster and avoid paying more than you should.

Seek Professional Help

Sometimes, handling medical bills and insurance feels like too much. You do not have to do it alone. Many professionals can guide you through the process and help you save money.

Financial Counselors

A financial counselor can make a big difference when you face medical costs after treatment. These experts know how to help you plan and budget for your bills. They can show you ways to use financial assistance programs from groups like the Susan G. Komen Foundation or The Pink Fund. If you need help with Medicaid or Medicare, a counselor can walk you through the steps to apply. You might also need to set up a payment plan with your hospital. A financial counselor can talk to the billing office for you and help you get a plan that fits your budget.

Here are some ways a financial counselor can help you:

Create a budget for your medical expenses

Find and apply for grants or nonprofit aid

Guide you through Medicaid or Medicare applications

Negotiate payment plans with providers

Help you apply for disability benefits if you cannot work

Tip: Ask your hospital or clinic if they have a financial counselor on staff. Many offer this service for free.

Patient Advocates

Patient advocates stand by your side when you deal with insurance and billing problems. They know how to read medical bills and spot mistakes. If you get a bill that looks wrong, a patient advocate can talk to the provider and ask for a lower charge. They can also help you apply for financial assistance programs or set up no-interest payment plans.

You might also hear about medical billing advocates. These professionals can:

Fix billing errors and negotiate lower rates

Work with debt collectors to make sure you get fair treatment

Help you understand your insurance and what it covers

Set up repayment plans or reduce your total bill

You do not have to face these challenges alone. Reaching out to a financial counselor or patient advocate can give you peace of mind and help you take control of your medical costs.

You can take charge of your medical bills by staying organized, asking questions, and reaching out for help when you need it. When you keep your paperwork in order, you feel calmer and less stressed. You save time and money because you know where everything is. Staying on top of things helps you avoid mistakes and gives you more confidence. Remember, you do not have to do this alone—support is always available.

FAQ

What should I do if I get a medical bill I can’t pay?

You can call the billing office and ask for a payment plan. Many hospitals offer no-interest options. You can also ask about discounts or charity care. Don’t ignore the bill—help is available if you reach out.

How do I appeal an insurance denial?

Start by reading your denial letter. Call your insurance company and ask why they denied your claim. Gather your medical records and write an appeal letter. You can ask your doctor to help. Keep copies of everything.

Can I get help with prescription costs?

Yes! Many drug companies and charities offer programs to lower your costs. Ask your doctor or pharmacist about these options. You can also check websites like NeedyMeds or GoodRx for discounts.

What records should I keep for medical bills?

Keep every bill, Explanation of Benefits (EOB), and letter from your provider or insurer. Use a folder or binder. Write down who you talk to and what they say. Good records help you solve problems faster.

This article is for educational purposes only and is not a substitute for professional medical advice. For more details, please see our Disclaimer. To understand how we create and review our content, please see our Editorial Policy.

See Also

Choroid Plexus Carcinoma: Recognizing Signs and Available Therapies

Duodenal Cancer: Identifying Symptoms and Treatment Options

Conjunctival Melanoma: Key Signs and Treatment Approaches

LGL Leukemia: Important Symptoms, Diagnosis, and Care Strategies

Lymphomatoid Granulomatosis: Symptoms and Treatment Insights

© 2026 Banish Cancer. Banish Cancer is a registered non-profit organization providing evidence-based research, educational courses, and Fear Response AI support services. Reg. No: 305706884 | Address: Taikos pr. 43-603, Kaunas, Lithuania.