Understanding Insurance and Healthcare Options Made Simple

Have you ever wondered how you would pay for a doctor’s visit or a hospital stay? Health insurance helps you manage these costs. It acts as a safety net, so you do not have to worry about big medical bills. You can choose from different healthcare options. Some people get insurance through work, others use government programs like Medicare or Medicaid. Here is a simple table to show the most common choices and what they cover:

Healthcare Option | Description | Coverage Details |

|---|---|---|

Private Insurance Plans | Includes national and regional plans, often employer-sponsored or individual. | Coverage varies; employers may cover part of premiums, and individuals can qualify for tax credits. |

Public Insurance Programs | Includes Medicare, Medicaid, and CHIP, funded by government taxes. | Medicare covers seniors and disabled; Medicaid assists low-income individuals; CHIP covers children. |

Understanding Insurance and Healthcare Options gives you the power to make smart choices for your health.

Key Takeaways

Health insurance protects you from high medical costs. It covers doctor visits, hospital stays, and more.

Know your plan's costs, like premiums and deductibles. This helps you budget for healthcare expenses.

Choose in-network providers to save money. Using out-of-network services can lead to higher bills.

Understand the different types of insurance plans. Each has unique rules about costs and provider access.

Use preventive services covered by your plan. They help you stay healthy and catch issues early.

Understanding Insurance and Healthcare Options

Health insurance serves as a crucial part of understanding insurance and healthcare options, providing financial protection when you face medical expenses. According to the Health Insurance Association of America, health insurance is defined as coverage that provides for the payments of benefits resulting from sickness or injury. This definition emphasizes that health insurance encompasses various types of coverage, and it establishes a contractual relationship between insurers and insured individuals. In simple terms, it means that when you sign up for a health plan, you agree to pay premiums, and in return, the insurance company agrees to cover certain medical costs.

What Is Health Insurance?

Health insurance acts as an umbrella for your medical needs. It covers costs related to accidents, illness, disability, and even accidental death. You pay a monthly premium, and the insurer helps pay for doctor visits, hospital stays, and other health services. The table below shows how major organizations define health insurance:

Source | Definition |

|---|---|

Health Insurance Association of America | "Coverage that provides for the payments of benefits as a result of sickness or injury. It includes insurance for losses from accident, medical expense, disability, or accidental death and dismemberment." |

Health insurance includes many types of coverage.

It creates a contract between you and the insurance company.

How Health Insurance Works

Your health insurance plan outlines what you pay and what the insurer covers. You may pay a deductible before your insurance starts to pay. You might also pay a co-payment for each doctor visit or coinsurance for part of a surgery. Some services, called exclusions, are not covered, so you pay the full cost. The insurer sets coverage limits and an out-of-pocket maximum, which protects you from very high bills. The table below explains these terms:

Term | Description |

|---|---|

Deductible | The amount you must pay out-of-pocket before the insurer pays its share. For example, a $7500 deductible must be met before coverage begins. |

Co-payment | A fixed amount you pay for a specific service, such as a $45 co-payment for a doctor's visit. |

Coinsurance | A percentage of the total cost you pay after a co-payment, e.g., 20% of surgery costs. |

Exclusions | Services not covered by the policy, where you pay the full cost. |

Coverage limits | Maximum dollar amount the insurer will pay for services, beyond which you are responsible for costs. |

Out-of-pocket max | The maximum amount you pay in a year, after which the insurer covers all further costs. |

In-Network Provider | Providers contracted with the insurer, offering lower costs for services. |

Out-of-Network Provider | Providers not contracted with the insurer, where you may pay full costs. |

Prior Authorization | Required approval from the insurer before certain services are provided, ensuring payment for authorized services. |

Tip: Always check if your doctor or hospital is in-network before you get care. This helps you avoid unexpected bills.

Why It Matters

Understanding insurance and healthcare options gives you control over your health and finances. Research shows that knowing your plan helps you make better decisions about care. You can avoid high costs by choosing in-network providers and using services that your plan covers. Studies like the Oregon Medicaid Experiment found that insurance increases medical service usage and improves your sense of well-being, even if it does not always change objective health measures. Medicare expansion studies also show that people feel happier and more secure when they have coverage.

Knowing your plan’s costs, like deductibles and co-pays, helps you plan for medical expenses.

Awareness of coverage rules encourages you to use preventive services, which can improve your health.

Understanding insurance and healthcare options helps you avoid surprise bills and supports your financial security.

When you understand your health insurance, you become an active participant in your care. You make informed choices, protect your finances, and improve your overall well-being.

Plan Types

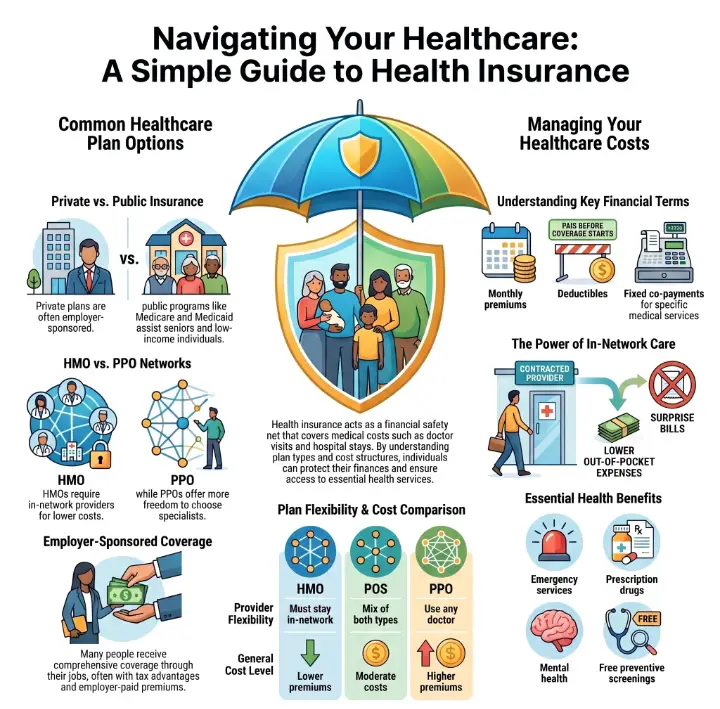

Private vs. Public Insurance

You can choose between private and public health insurance. Private insurance comes from companies. You may get it through your job, buy it yourself, or use special programs like TRICARE. Public insurance includes programs like Medicare and Medicaid. These programs use taxpayer money and help people who meet certain rules, such as age or income. Public insurance often covers basic health needs for at-risk groups.

Here is a quick look at how many Americans use each type:

Insurance Type | Coverage Percentage |

|---|---|

Private Insurance | |

Public Insurance | 35.5% |

Private insurance covers most people. Public insurance helps those who need extra support.

Common Plan Types (HMO, PPO, EPO, POS)

You will see different plan types when you look at insurance. Each plan has its own rules for doctors, costs, and how you get care. The table below shows the main differences:

Plan Type | Network Flexibility | Cost Structure |

|---|---|---|

HMO | You must use in-network providers. No coverage for out-of-network care. | Lower premiums and out-of-pocket costs. Less choice. |

PPO | You can see any doctor. No referrals needed for specialists. | Higher premiums. More freedom to choose providers. |

EPO | Like a PPO, but no out-of-network coverage. | Lower costs than PPO. Must stay in network. |

POS | Mix of HMO and PPO. Referrals needed for specialists. | Moderate costs. Higher if you go out-of-network. |

Tip: If you want to keep your doctor, check if they are in the plan’s network before you sign up.

Pros and Cons

Every plan type has good points and bad points. HMOs cost less but limit your choices. PPOs give you more freedom but cost more. EPOs offer lower prices but require you to stay in the network. POS plans let you go out-of-network, but you pay more and need referrals.

Understanding Insurance and Healthcare Options helps you pick the plan that fits your needs and budget. You can balance cost, choice, and coverage when you know the basics.

Key Terms and Benefits

Premiums, Deductibles, Copays, Coinsurance

You pay for health insurance in several ways. The main costs include premiums, deductibles, copays, and coinsurance. Each one affects how much you spend on healthcare.

In 2025, the average worker paid $1,440 a year for single coverage and $6,850 for family coverage as their share of the premium.

The average deductible for single coverage was $1,886. Workers at smaller companies often paid more.

Deductibles made up over half of what people paid out-of-pocket.

The Affordable Care Act sets a limit on how much you pay out-of-pocket each year. Once you reach this maximum, your plan pays 100% of covered costs. People with high health needs pay the most. The top 1% of spenders paid about $23,700 out-of-pocket in 2022, while half of people paid only $24.

Networks and Coverage

Your insurance plan has a network of doctors and hospitals. You save money by using providers in your network. Networks are built to match your needs, including location, appointment times, and even cultural preferences.

Provider Type | Coverage Level | Patient Cost Implications |

|---|---|---|

In-Network Provider | Higher coverage, lower out-of-pocket costs | Generally lower costs for services received |

Out-of-Network Provider | Lower coverage, higher out-of-pocket costs | Patients may pay full costs and additional fees for services |

A well-managed network helps you get care more easily and keeps your costs down.

Essential Health Benefits

All major health plans must cover a set of essential health benefits. These benefits protect you from big medical bills and make sure you get important care.

Essential Health Benefits |

|---|

Ambulatory patient services |

Emergency services |

Hospitalization |

Pregnancy, maternity, and newborn care |

Mental health and substance use disorder services |

Prescription drugs |

Rehabilitative and habilitative services and devices |

Laboratory services |

Pediatric services (including oral and vision care) |

Total birth control coverage |

Breastfeeding coverage |

Research shows that insurance gives you peace of mind and protects your finances. It may not always improve your health, but it helps you feel more secure.

Preventive Services

Most health plans cover preventive services at no extra cost to you. These services help you stay healthy and catch problems early.

Immunizations

Cancer screenings

Cholesterol checks

Counseling for healthy eating or quitting smoking

Tip: Use your preventive services every year. They can help you avoid bigger health problems later.

Healthcare Coverage Options

When you look for health insurance, you will see several main options. Each one works differently and fits different needs. Understanding Insurance and Healthcare Options helps you choose the best path for your health and budget.

Employer-Sponsored Insurance

Many people get health insurance through their jobs. Your employer may offer a plan and pay part of the cost. You pay the rest, usually through payroll deductions. These plans often give you a wide range of coverage and can include dental or vision benefits. You may also get tax advantages because your premiums come out of your paycheck before taxes.

Here is a table that shows some common benefits and limitations of employer-sponsored insurance:

Benefits | Limitations |

|---|---|

Comprehensive coverage options | Potential uneven coverage for low-wage workers |

Tax advantages | Financial burden of premiums and cost-sharing for employees |

Risk management efficiencies | N/A |

Note: If you change jobs or lose your job, you might lose your coverage. You can use COBRA to keep your plan for a short time, but it often costs more.

Government Programs (Medicare, Medicaid)

The government offers health insurance for people who meet certain rules. Medicare helps people who are 65 or older or have certain disabilities. Medicaid helps people with low income. These programs cover many basic health needs, such as doctor visits, hospital stays, and prescription drugs. You may pay little or nothing for care if you qualify.

Tip: Check if you qualify for these programs. They can save you money and give you peace of mind.

Individual and Marketplace Plans

If you do not get insurance from a job or the government, you can buy your own plan. The Health Insurance Marketplace lets you compare plans and prices. You may get help paying for your plan if your income is low or moderate. These plans must cover essential health benefits, like doctor visits and preventive care.

You can shop for plans during open enrollment or after certain life events, such as losing other coverage. Marketplace plans give you control over your choices and let you pick what fits your needs.

Understanding Insurance and Healthcare Options means you can find the right coverage for your life. You can protect your health and your wallet by knowing your options.

Choosing the Right Plan

Selecting the right health insurance plan can feel overwhelming. You can make a smart choice by breaking the process into simple steps. This section will guide you through assessing your needs, comparing costs and coverage, checking provider networks, and making your final decision.

Assessing Your Needs

Start by thinking about your health and your family's needs. Consider how often you visit the doctor, what prescriptions you take, and if you expect any surgeries or special care. Make a list of your regular healthcare expenses. This helps you see what kind of coverage you need.

Here are some important factors to consider:

Understand all costs, including monthly premiums and out-of-pocket expenses.

Evaluate coverage options, such as which doctors and services the plan covers.

Look for preventive care benefits, which many plans cover at no extra cost.

Review plan details, including deductibles and copayments.

Make sure your doctors and local hospitals are in the plan's network.

Confirm if the plan covers your spouse and dependents.

Read all plan materials to know your rights and responsibilities.

Check for any rules about pre-existing conditions or prior authorizations.

Tip: Write down your main health needs before you start comparing plans. This keeps you focused on what matters most.

Comparing Costs and Coverage

Next, compare the costs and coverage of different plans. Look at the monthly premium, but also check how much you pay when you get care. Plans with lower premiums may have higher deductibles or copays. Plans with higher premiums may cover more services with less out-of-pocket cost.

You can use online tools to help compare plans. For example, the Health Insurance Marketplace lets you see side-by-side comparisons. The Ohio Department of Insurance suggests looking at your healthcare costs from past years. This helps you estimate what you might spend in the future. The Illinois Department of Insurance also recommends using the Marketplace to find out if you qualify for premium tax credits, which can lower your costs.

Cost Type | What to Check |

|---|---|

Premium | Monthly payment for the plan |

Deductible | Amount you pay before coverage starts |

Copayment | Fixed fee for each visit or service |

Coinsurance | Percentage you pay after deductible |

Out-of-pocket max | The most you will pay in a year |

Note: Always look beyond the premium. A plan with a low monthly cost may end up costing more if you need a lot of care.

Checking Provider Networks

Provider networks are groups of doctors, hospitals, and clinics that work with your insurance plan. Using in-network providers saves you money. Out-of-network care usually costs more or may not be covered at all.

Check if your favorite doctors and local hospitals are in the plan's network. If you have a specialist you see often, make sure they are included. Some plans require you to get referrals to see specialists. Others let you go directly.

Search the plan’s website for a list of in-network providers.

Call your doctor’s office to confirm they accept the plan.

Look for nearby hospitals and urgent care centers in the network.

Tip: Staying in-network helps you avoid surprise bills and keeps your costs lower.

Making Your Decision

After you gather all the information, you are ready to choose a plan. Review your notes about your health needs, costs, and preferred providers. Think about which plan fits your budget and covers the care you need.

Here is a simple step-by-step guide:

List your health needs and regular expenses.

Compare plans for costs and coverage.

Check if your doctors and hospitals are in-network.

Read the plan’s rules and benefits.

Choose the plan that matches your needs and budget.

Remember: The best plan for you balances both coverage and cost. Take your time, ask questions, and use online resources to help you decide.

Choosing the right health insurance plan puts you in control of your health and your finances. You can feel confident knowing you made an informed choice.

You now know the basics of health insurance and your coverage options. Review your needs, compare plans, and check which doctors are in-network. This knowledge helps you make smart choices for your health and money.

List your top health needs.

Compare costs and coverage.

Ask questions if you feel unsure.

Tip: Use online tools or talk to an insurance expert to help you pick the best plan for you.

FAQ

What if I miss the open enrollment period?

You can only sign up for health insurance during open enrollment. If you miss it, you may qualify for a special enrollment period if you have a big life change, like losing your job or having a baby.

Can I keep my doctor with a new plan?

Check if your doctor is in the new plan’s network. Most insurance companies have a list of in-network doctors on their website. If your doctor is not in-network, you may pay more or need to choose a new provider.

What does “out-of-pocket maximum” mean?

Your out-of-pocket maximum is the most you will pay for covered services in a year. After you reach this amount, your insurance pays 100% of covered costs for the rest of the year.

Do all plans cover prescription drugs?

Most health insurance plans cover prescription drugs, but coverage can vary. Always review the plan’s drug list, called a formulary, to see if your medicine is included and how much you will pay.

This article is for educational purposes only and is not a substitute for professional medical advice. For more details, please see our Disclaimer. To understand how we create and review our content, please see our Editorial Policy.

See Also

Simplifying B-Cell Prolymphocytic Leukemia For Better Understanding

An In-Depth Overview Of Every Cancer Type Available

Understanding Insulinoma: Its Importance And Key Facts

© 2026 Banish Cancer. Banish Cancer is a registered non-profit organization providing evidence-based research, educational courses, and Fear Response AI support services. Reg. No: 305706884 | Address: Taikos pr. 43-603, Kaunas, Lithuania.